Education

New episodes, articles and listings weekly!

- All

- Financial Literacy

- Meet The Clients

- Videos

Clay and Alex Gilmer

They are a hardworking couple, crushing life. Their next adventure is buying their 2nd property and they…

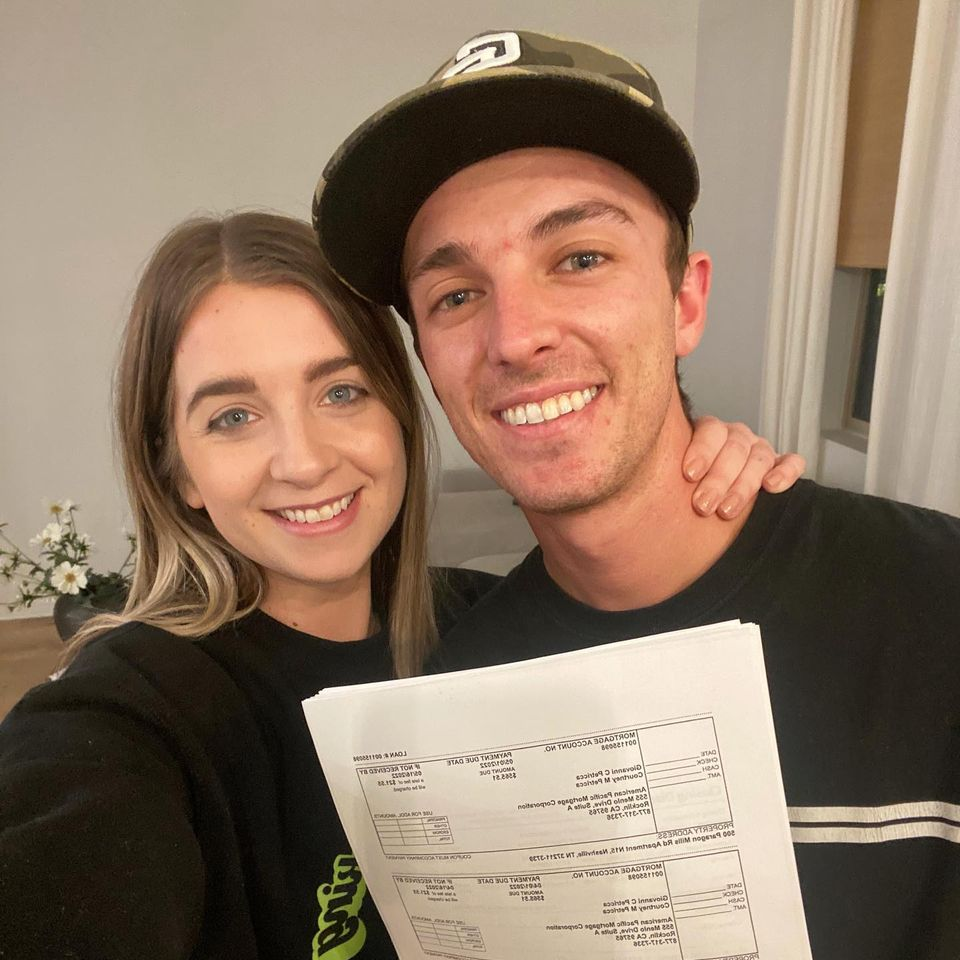

Giovanni and Courtney

Meet my Clients Giovanni & Courtney Petricca! They currently live in CA & bought their 2nd property…

John and Christian Johansen

This 6 unit was acquired by a Father & Son duo from New York. They wanted an…

Raul and Ashley

Raul and Ashley Reutov put in some sweat equity in their previous property which allowed them to…

Will and Amanda

This one was special. Will and Amanda Mortimore tried 9 times to go under contract before landing…

Jordan, Morgan and Laith Parton

This one was about perseverance! We had close calls and no dice with several of our offers….

Shane Gardner

For years, Shane was interested in owning his own place. Not only that, but he also wanted…

Mike and Justine

Their story is a special one. Mike and Justine are getting married and knew they wanted to…

Alex and Lindsay

They are the definition of taking action. Alex and Lindsay wanted to take control of their lives,…

FAQs

House hacking is the practice of purchasing a property and living in it while renting out part or all of the property to others in order to offset living expenses. It is a strategy used by real estate investors to save money on housing costs and build wealth through property ownership.

Debt-to-income (DTI) ratio is a financial measurement that compares the amount of debt an individual has to their monthly income. It is used by lenders to evaluate a borrower's ability to repay a loan and is an important factor in the lending decision process. A lower DTI ratio is generally considered better, as it indicates that a borrower has a lower burden of debt and is more likely to be able to make their loan payments.

The amount of money needed for a down payment on a primary residence loan can vary. Generally, lenders require a down payment of at least 3% of the purchase price of the home, but some lenders may require a larger down payment. However, there are also programs available that allow for a lower down payment or even no down payment at all. It's important to speak with a lender to determine the specific down payment requirements for the loan you are seeking.

Using a realtor can be beneficial for several reasons. Realtors are licensed professionals who are trained in the real estate industry and are knowledgeable about the local market. They can help you navigate the process of buying or selling a home, including finding properties that meet your specific needs and budget, negotiating offers and contracts, and managing the closing process. Realtors also have access to a network of resources and tools that can be useful in the home buying or selling process.

There are several reasons why one might consider buying a home even if they plan to move in the near future. For example, if a person is moving to a new city or country for a job, they may still want to purchase a home in their current location in order to take advantage of low mortgage rates and potentially build equity in the property. Additionally, if a person expects to move back to their current location in the future, buying a home can allow them to have a place to return to rather than starting from scratch when they return. Additionally, if the person expects property values in their current location to appreciate significantly, owning a home could provide a good financial investment. It's important to carefully consider the individual's specific circumstances and goals when deciding whether to buy a home.

Having debt does not necessarily prevent a person from buying a house. In fact, many people have debt when they purchase a home. When evaluating a loan application, lenders will consider the borrower's debt-to-income (DTI) ratio, which is a measure of the borrower's monthly debt payments compared to their monthly income. As long as the borrower's DTI is within a lender's acceptable range and the borrower meets other lending requirements, such as having a good credit score and sufficient income, they may still be approved for a mortgage. It's important to work with a lender to understand the specific requirements and to determine the best course of action for managing debt while also pursuing homeownership.

The ease of buying property can vary depending on several factors, such as the individual's financial situation, the availability of properties in the desired location, and market conditions. In general, the process of buying property involves several steps, including finding a property, negotiating a purchase price, obtaining financing, and completing the closing process. Some people may find the process to be relatively straightforward, while others may encounter challenges along the way. Working with a realtor and a lender can help make the process smoother and more efficient.